Every macro trend for Peloton and PTON stock in 2020 could not be more favorable. In terms of the macro scenario, last year was at best a mediocre year for the exercise-equipment manufacturer. Late last year, the company’s and its stock’s fortunes started to deteriorate. All indications now point to Peloton and the stock repeating its 2020 performance.

To put it another way, every imaginable macro trend appears to be working against the company. As a result, now is not the time to purchase or even hold PTON shares. Peloton is temporarily suspending production of its connected fitness products as demand declines and the business seeks to cut costs.

According to the documents, Peloton plans to suspend Bike production for two months, from February to March. It stopped producing its more expensive Bike+ in December and will continue to do so until June. Beginning next month, it will stop producing its Tread treadmill machine for six weeks. According to the records, it does not plan to produce any Tread+ machines in fiscal 2022. Tread+ production had previously been halted by Peloton following a safety recall last year.

Due to shoppers’ price sensitivity and increased competition activity, the business said in a confidential presentation dated Jan. 10 that demand for its connected fitness equipment has seen a “significant reduction” around the world.

After so much demand was moved forward during the coronavirus outbreak, Peloton effectively got it wrong about how many people would be buying its products. Thousands of cycles and treadmills are now lying in warehouses or on cargo ships, and the company has to reset its inventory.

Peloton’s market cap has been slashed by over $40 billion in the last year, prompting the scheduled production halt. Its market capitalization peaked at roughly $50 billion in January.

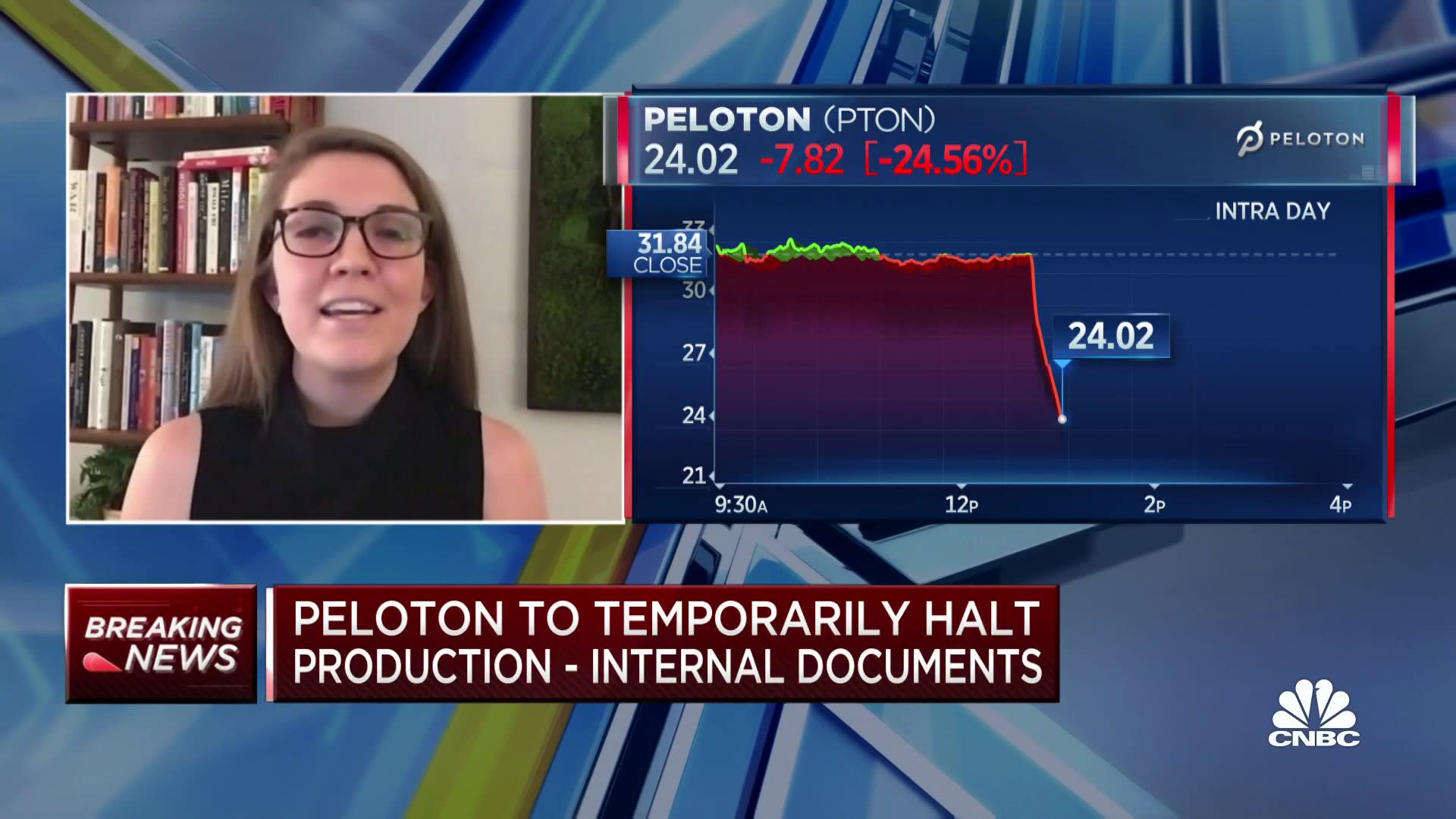

Peloton shares fell 23.9 % to $24.22 on Thursday, bringing the stock’s market worth to $7.9 billion. The stock hit a 52-week low of $23.25 during the trade. The stock also fell below $29, where it was priced ahead of Peloton’s initial public offering.

Peloton’s presentation demonstrates that on Oct. 31, the company established expectations for demand and deliveries in its fiscal third and fourth quarters that were substantially too high. According to the presentation, it reevaluated those predictions on Dec. 14, and Peloton’s expectations for its Bike, Bike+, and Tread products dropped significantly.

The Effects of Recent Trends on Peloton Stock

Peloton and its stock have recently underperformed in line with common sense, as the 2022 trends we highlighted above have begun to materialize.

Peloton’s “website visits and page views declined Y/Y in December (month-to-date),” according to JMP Securities on Dec. 31. The information came from Similarweb, according to the firm.

As a result of this data, the company reduced its predictions for Peloton’s fiscal year 2022, which are now lower than analysts’ predictions and Peloton’s guidance.

On the same day, Raymond James, a research firm, claimed that “our analysis of search data continued to show a meaningful year-over-year slowdown” for Peloton. The firm maintains a “market perform” rating on the stock because it believes the company will miss its guidance.

Peloton’s fiscal first-quarter results, which were revealed on November 4, were likewise poor. The company posted $1.25 earnings per share in the first quarter, which was 17 cents lower than analysts’ estimates. In addition, revenue increased only 6.2 % year over year to $805.2 million, below the mean estimate by $3.67 million.

Peloton also reduced its FY22 topline target to $4.4 billion to $4.48 billion, down from $5.4 billion previously. Meanwhile, the business now estimates full-year EBITDA of -$425 million to -$475 million, excluding certain factors.

Continue Reading:

US Inflation at an All Time High 2022